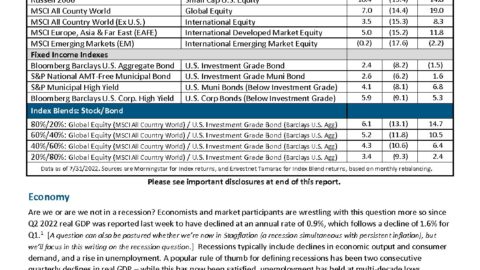

2017 Review & 2018 Preview

By Steven Higgins, Financial Advisor

In Review: Top Stories Affecting Our Clients In 2017

1. Record low downside volatility leads to significant gains in stocks.

U.S. stock markets experienced record low adverse days in 2017. Dana Lyons, the editor of The Lyons Share took a creative look at the details. When compiling all of the down days in the DOW Jones Industrial Average over the course of the year, Lyons found that in the past 100 years 2017 had less adversity than any other year with  cumulative down days equaling (27%). The only year to even come close was 1965 with (31%). The average year experiences cumulative losses on negative days of 90%. The net result of 2017 for the Dow Jones Industrial Average was a gain of 25%.

cumulative down days equaling (27%). The only year to even come close was 1965 with (31%). The average year experiences cumulative losses on negative days of 90%. The net result of 2017 for the Dow Jones Industrial Average was a gain of 25%.

Source: Lyons Share Post

2. Tax bill is signed, paving way for a new generation of tax laws.

The Republican-controlled House and Senate along with President Trump overcame the infighting that had plagued them for much of 2017. On December 19, the President signed the tax bill into law. The New York Times said, “The $1.5 trillion bill represents the most sweeping overhaul of the United States tax code in decades, delivering deep and permanent cuts to corporations and temporary tax cuts to individuals.”

The tax plan relies on the long held Republican tenant that lower taxes will fuel economic growth. While early polls show much of the public is leery of the concept, only time will tell if the plan is a success.

Source: NY Times Article

3. Home prices continue the upward trajectory.

According to the the S&P Corelogic Case-Schiller Indices, Denver home prices increased year over year by 7.2% in October. National average of 20 major cities was an increase of 6.4%. Seattle came in first with price increases averaging 12.7%. Lack of supply seems to be the key driver of the the increase. An October 2017 report from coloradorealtors.com says that the current Denver Metro Housing Supply is 1.7 months down 34% from last year.

“The last few months of 2017 have clearly demonstrated the extent to which the housing market refuses to be knocked off its stride,” Zillow senior economist Aaron Terrazas said. “Whether and how long the housing market can continue to defy gravity, and whether the good times last into 2018, remain open questions. But for now, the fundamentals driving the market today look unlikely to change any time soon.”

Source: Denver Post Article

4. Fed increased interest rates three times, signaling increased borrowing costs are in the near future.

In December, the Federal Reserve increased the benchmark Fed Funds Rate from 1.25% to 1.5%. The increase marked the 3rd time in 2017 that the Fed increased rates. The meeting also served as somewhat of a swan song for outgoing Fed Chair Janet Yellen as she will be leaving her post. The Federal Reserve changes the federal funds rate to control money supply and inflation. In times of low growth or recession the rate can be lower to facilitate easier access to money. In times of high growth or high inflation, the rate can be higher to keep things from getting over heated. The highest the rate has ever been was 20% in 1979. The lowest the rate has ever been was 0.25% in 2008. The Fed maintained the record low rate of 0.25% for 7 years until increasing it in 2015.

In December, the Federal Reserve increased the benchmark Fed Funds Rate from 1.25% to 1.5%. The increase marked the 3rd time in 2017 that the Fed increased rates. The meeting also served as somewhat of a swan song for outgoing Fed Chair Janet Yellen as she will be leaving her post. The Federal Reserve changes the federal funds rate to control money supply and inflation. In times of low growth or recession the rate can be lower to facilitate easier access to money. In times of high growth or high inflation, the rate can be higher to keep things from getting over heated. The highest the rate has ever been was 20% in 1979. The lowest the rate has ever been was 0.25% in 2008. The Fed maintained the record low rate of 0.25% for 7 years until increasing it in 2015.

*Data sourced from St. Louis Federal Reserve Bank

5. Inflation silently picking up pace, increasing cost of living.

We keep hearing that inflation remains an economic “non-issue.” Fed Chair Woman Janet Yellen even expressed surprise at the lack of inflation. Our experience as financial advisors has been quite different. Our clients are facing increasing cost in every facet of their lives. The reason for the difference is the perspective. Economists are essentially taking the current temperature of classic economic indicators while our clients who are essentially retirees and pre-retirees are living life. Housing costs – including the price of homes, cost of insurance, and property taxes – along with health care costs have increased dramatically. While the calculations of the government economic data can be complicated, inflation doesn’t have to be. Both Netflix* and Starbucks** increased prices by over 10% in 2017.

We keep hearing that inflation remains an economic “non-issue.” Fed Chair Woman Janet Yellen even expressed surprise at the lack of inflation. Our experience as financial advisors has been quite different. Our clients are facing increasing cost in every facet of their lives. The reason for the difference is the perspective. Economists are essentially taking the current temperature of classic economic indicators while our clients who are essentially retirees and pre-retirees are living life. Housing costs – including the price of homes, cost of insurance, and property taxes – along with health care costs have increased dramatically. While the calculations of the government economic data can be complicated, inflation doesn’t have to be. Both Netflix* and Starbucks** increased prices by over 10% in 2017.

Sources: forbes.com* CNN.com**

Looking Forward: Top Stories That May Affect Our Clients In 2018

1. Change to tax laws will impact how some clients will file their taxes and how much they pay.

You may be a fan of the new Republican tax bill or you may not, but either way it will affect you. While the tax rates have come down, and the standard deduction has been doubled, there have been limits put on certain deductions and the personal exemptions have gone away. For some self employed folks who pass through their business income to their individual return, there may be some relief.

One of the big headline grabbing items was a reduction of the corporate tax rate from 35% to 21%. While few corporations were actually paying the statutory 35% rate, the reduction will certainly have some positive impact on the bottom line. While some argue the reduction in the corporate rate was just a gift to enrich companies, there may be benefits for share holders of those companies. So if you own stocks, the reduction in the corporate rate should be seen as a good thing for you. Danielle Kurtzleben of NPR writes in her August 2017 article about global corporate tax rates, “The U.S. has the highest top corporate tax rate at least among advanced economies. Compared with nations in the OECD — the Organization for Economic Cooperation and Development, a group of highly developed countries — the U.S. has the highest top corporate tax rate in the world. The top corporate tax rate in the U.S., a combination of federal and state and local taxes, is nearly 39 percent this year. That’s well above most other OECD nations.”

Companies like Southwest and American Airlines, AT&T, and Comcast have already issued $1,000 bonuses to all employees to celebrate the tax cut. Wells Fargo announced that because of the tax cut they will increase their minimum wage to $15 an hour. While the bonuses can be seen as a tad bit pandering they still represent real money for many employees that haven’t seen significant wage increases for a long time.

A word of caution regarding the new tax plan. The passage of this tax plan, not unlike the entire year of 2017 has been hyper politicized. While there is no shortage of comments and quips from those on both sides, I would suggest that few really understand how this plan will affect them. Our recommendation to clients now that the political smoke is clearing is this: spend less time worrying about the macro shortcomings and blessings of the plan and figure out how to make it work best for you.

Source: NPR Article

2. Historic bond bull market may be coming to an end.

Over the last three decades the bond market has earned a reputation as the safe way to create wealth. Consistently declining interest rates have driven up and stabilized the prices of bonds. With interest rates only recently bouncing back from record low levels, bonds are facing their first real test. Increasing interest rates causes the value of existing bonds to fall and investors may face significant challenges with what they imagined was the “predictable” part of their portfolio. At HD Wealth Strategies we continue to advise clients to prepare for rising interest rates and re-think the “bond” part of their portfolios.

Relevant Note: It is not lost on me that 2018 marks ten years since the Federal Reserve lowered their benchmark rate to a record low 0.25%. Also, 2008 was the beginning of the stimulus barrage that was highlighted by a multi-year and multi-trillion dollar bond buying program. These programs aimed at invigorating a wounded economy perpetuated an already historic bull market in bonds.

Relevant Note: It is not lost on me that 2018 marks ten years since the Federal Reserve lowered their benchmark rate to a record low 0.25%. Also, 2008 was the beginning of the stimulus barrage that was highlighted by a multi-year and multi-trillion dollar bond buying program. These programs aimed at invigorating a wounded economy perpetuated an already historic bull market in bonds.

In the summer of 2013 I wrote a letter to clients in response of the “taper-tantrum” that ensued when then Fed Chairman, Ben Bernanke warned that the Fed may begin to slow down their bond buying program. The bond market took a pretty severe hit and people thought that interest rates would skyrocket.

“…we will face intermittent fear and corresponding volatility while the Fed attempts to sneak the elephant out of the room. This may take a while. It is a historically large elephant.” (SH – Letter to clients June 28, 2013.)

Five years later, they are still working on the whole elephant thing

3. Earnings growth and available cash may drive stocks to more record highs.

The fourth quarter of 2017 will mark the fifth consecutive quarter of earnings growth in the S&P 500. This streak follows the previous seven consecutive quarters of earnings decline. The robust earning growth growth legitimatizes the gains in stock. In short, stocks deserve the gains. The question is can stocks continue the record path higher? If earnings continue to to grow, there is plenty of cash in the system to bid stock prices higher. Almost a decade of federal stimulus equaling nearly $7 trillion dollars, a recent tax cut for both individuals and corporations, and a robust job market can help provide the fuel for continued stock market gains. As always it’s easy to plan for the things we know, it’s the things we don’t know that can surprise us. With the reality of market history as our guide, we implore to maintain balance and diversity in portfolios. There is never a smart time to be “all in.”

4. Inflation may pick up the pace, surprising many investors.

Most of the current investing public has never lived in a period of time when inflation was a significant part of their investing narrative. 35 years ago we ended what was the last long term period of high inflation. From 1973 to 1983, inflation averaged 8.75% per year, essentially reducing the spending power of every dollar to 43 cents.* Over the last ten years the U.S. has doubled the amount of money in the system and the U.S. population has become very willing to accept a continued, massive supply of stimulus in the form of tax cuts, bailouts, social programs, infrastructure programs, and so on. Throw in potential repatriation of currency by major U.S. companies stock piling cash overseas and you have the stage for significantly more money chasing a supply of goods and services that simply will not keep up.

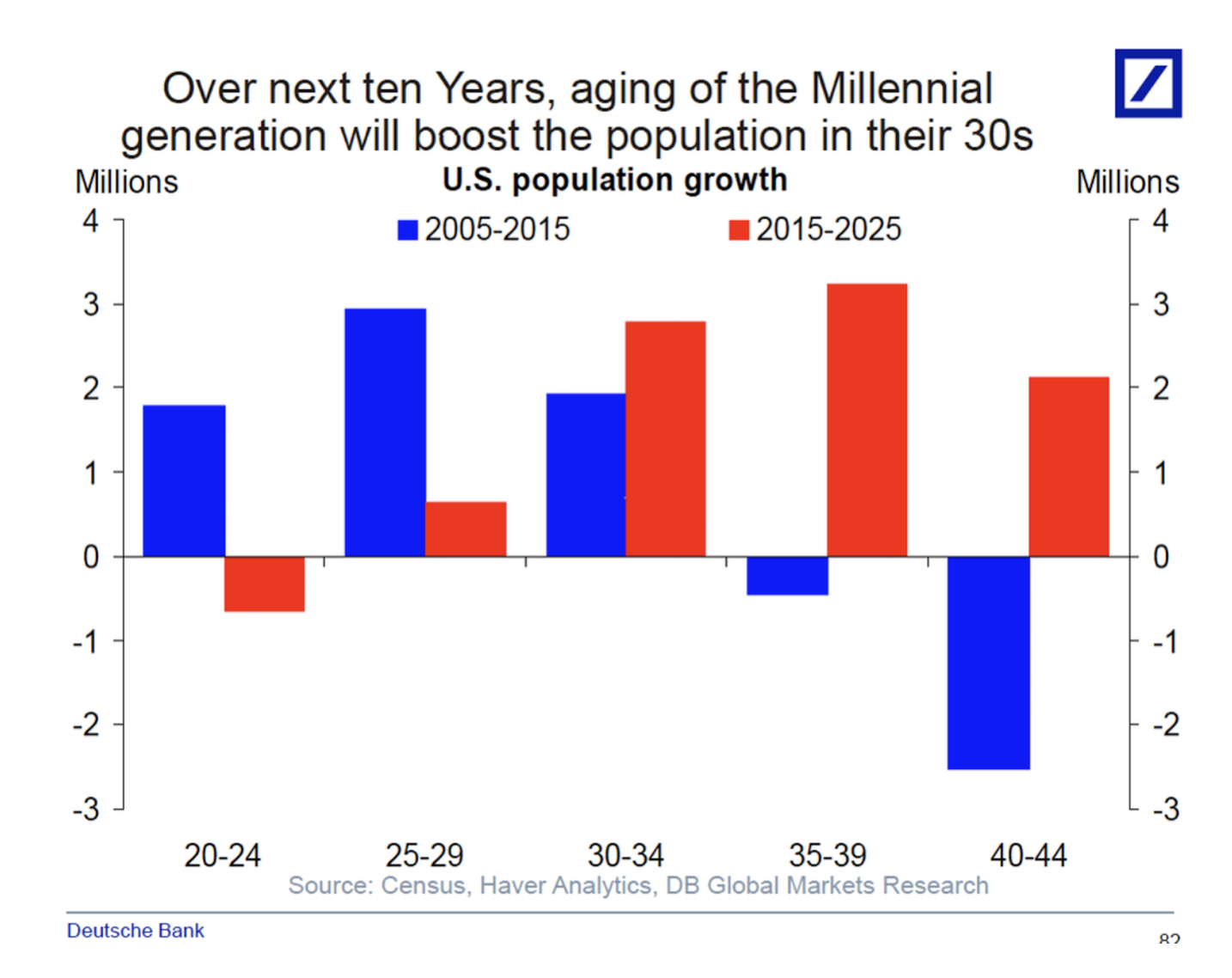

As if the recipe for inflation was lacking any other ingredients, consider this: people become economically formidable when they begin the process of “Household Formation.” They earn more, spend more, have families and buy bigger homes and second cars. Yes, those millennials are growing up.

Investors may be dissuaded from the belief that days of higher inflation are ahead considering all of the talk in the media about current, low levels of inflation. We caution our clients to think of their investing plan like any good long road trip; you might not want to stare at the speedometer the whole time. What’s important is what’s down the road a bit.

Inflation may be a really good thing for a portfolio or really bad, it just depends on whether you are prepared for it.

*Source: Bureau of Labor & Statistics (www.bls.gov)

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly. The opinions expressed in this material do not necessarily reflect the views of LPL Financial. The economic forecasts set forth in this material may not develop as predicted and there can be no guarantee that strategies promoted will be successful. There is no guarantee that a diversified portfolio will enhance overall returns or outperform a non-diversified portfolio. Diversification does not protect against market risk. All investing, including stocks, involves risk including loss of principal. Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price. The Dow Jones Industrial Average is comprised of 30 stocks that are major factors in their industries and widely held by individuals and institutional investors. Any named entity, HD Wealth Strategies, and LPL Financial are not affiliated. This information is not intended to be a substitute for specific individualized advice. We suggest that you discuss your specific tax issues with a qualified tax advisor.

{kind=link}

{kind=link}