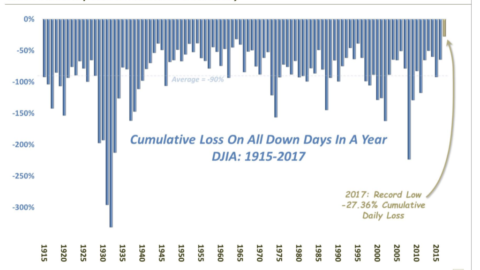

Is Twenty the New Forty?

Another Look at Asset Allocation

By Allison Schmidt, Financial Advisor, CFP®, CPA

Historically, asset allocation was pretty straight forward: you had a portion in stocks for growth and a portion in bonds for stability, such as the popular 60/40 (60% stocks, 40% bonds). You rebalanced that once a year, and over the last 30 years, you would have returned about 8%*…not too shabby! You were even able to avoid visiting the heart wrenching depths of the stock market bottoms in 2002 and 2009. Your portfolio during those times no doubt declined in value, but nothing compared to those taking on 90% or 100% stock exposure. But, times are different now. I would argue (and not many people disagree) that the next significant move for interest rates is up. (Bonds 101: if interest rates rise, bond prices fall. This scenario is the opposite of the last 30 years: interest rates dropped, so bond prices rose, contributing to your 60/40 return of 8%.) Interest rates are currently sitting close to historic lows. This fact magnified by our anticipation of higher than average inflation is why I’m recommending investors to take a closer look at the bond portion of their asset allocation and here’s why:

One word, inflation. It’s baaaccckkk. Since 2009, we have averaged under 1.5%^ inflation per year, less than half of the historic average of around 3%^. Remember quantitative easing or QE? This was when the Federal Reserve tried to help jump start the economy as we were trying to emerge from the Great Recession, and unemployment was upward of 10%**. This program consisted of the Fed purchasing bonds from banks, with the intention of lowering the interest rate and putting more cash into circulation or increasing the money supply; however, with increased regulation and historically low interest rates, the banks didn’t lend—they held onto the cash (shown with increasing M2). Banks’ balance sheets just got bigger, and it’s hard to blame them for not lending. It didn’t make sense for the bank to take any risk on lending to anyone who had less than stellar credit at such low rates—they just weren’t being paid to take the risk. Would you lend someone money, who has a less than perfect track record of paying back debts, for 30 years at 3%? No, probably not, but would you at 8%? You might consider it.

How does the money get into the system? We think this could happen in a couple ways that could create almost the perfect increased inflation storm. The Fed has let us know that we will likely see about three rate hikes in 2017, so increasing interest rates…check. Potential deregulation…check. Both measures would encourage banks to lend. The White House has discussed increased infrastructure spending and possible reduction in individual/corporate tax rates, so people will have more cash to spend…check.

So, if inflation is coming and maybe coming more quickly than we thought six months ago, what do you do? From an asset allocation standpoint, we suggest simply consider owning things that inflate and minimize what does not, such as bonds and cash. The old 60/40 allocation is outdated and could be downright dangerous with impending rising rates, inflation, and how much longer everyone is living. We need our money to last and to keep its spending power. Reevaluate the 40% and take a look at other non-correlative assets that could provide the benefits that bonds once did, income & principal stability, both of which are at stake today.

Inflation is powerful and something you don’t want to miss. A cup of coffee that costs $2.50 today goes to $4 in a couple years, and there’s not much chance it costs $2.50 ever again (even shown locally in the housing price increase in Colorado).

We’re not in the business of predicting whether markets will go up or down over short-periods of time, so please don’t confuse this with a market call. This is anticipating a longer term trend to be prepared for. Our goal is to help our clients focus on their financial goals, build portfolios that are well-diversified to weather market moves, give credence to economic realities, and prevent them from outliving their money. There is no question decreasing the predictability of a portfolio (bonds & cash) will increase volatility in your portfolio, both positive and negative. Be sure to meet with your financial advisor to discuss what is appropriate for you financially and emotionally. Investing and volatility can be a lot like riding a roller coaster—once you’ve started, it’s never advisable to hop off in the middle.

For more in-depth analysis on this topic, such as historic inflation, M2, and the Federal Reserve graphs, please check out my partner, Steven Higgins’s article “Inflated Expectations: A Cause for Concern or Optimism” on our blog at www.hdwscolorado.com/blog.

* 60% S&P500(TR) Index/40% Barclays U.S. Aggregate Bond Index

^ Source: CPI

** Source: Bureau of Labor Statistics

Securities offered through LPL Financial, Member FINRA/SIPC. Investment advice offered through HD Wealth Strategies, a registered investment advisor and separate entity from LPL Financial. The opinions voiced in this material are for general information only and are not intended to provide specific advise or recommendations for any individual. All performance referenced is historical and no guarantee of future results. There is no guarantee that a diversified portfolio will enhance overall returns or outperform a non-diversified portfolio. Diversification and asset allocation does not ensure a profit or protect against a loss. Stock investing involves risk including loss of principal. Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price. Rebalancing a portfolio may cause investors to incur tax liabilities and/or transaction costs and does not assure a profit or protect against a loss.